2025 Unicorns Class

Bonus: an interactive dashboard!

Unicorns (startups valued at $1B or more) signal success for founders, investors, and ecosystems. They’ve become a metric for measuring ecosystem health, policy effectiveness, founder grit, and investor competence. Since 2000, nearly 3,000 companies have reached unicorn status across more than 420 cities worldwide, according to Dealroom data. Almost half of companies valued at $1B or more remain private and venture-backed. Every year since 2018 has produced more than 100 new unicorns.

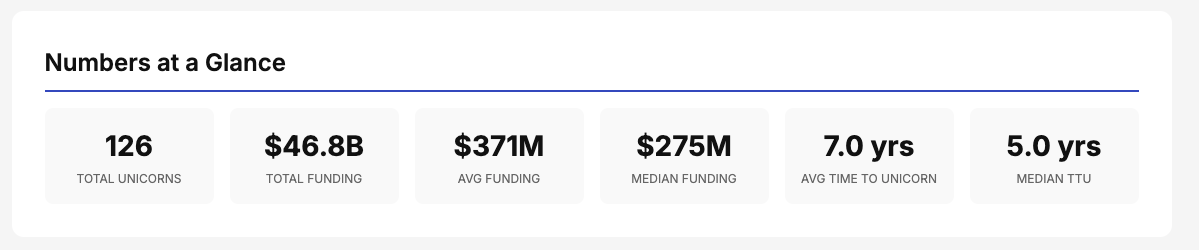

We analyzed 126 companies that reached unicorn status in 2025. Our analysis reveals three dominant themes:

AI has become the foundation layer of the entire cohort (duh!)

DeepTech is experiencing a renaissance driven by space, quantum, semiconductor and AI infrastructure investment

Time to unicorn has compressed dramatically - ****21% of companies achieved status in less than two years.

To complement this analysis, we've built an interactive data explorer — 2025 Unicorn Intelligence — where you can slice the full dataset by sector, geography, founding cohort, funding range, and more. Every chart in this article is static by design, meant to support a narrative. The dashboard, on the other hand, is designed for curiosity: filter for instant unicorns, compare capital intensity across verticals, or drill into the company directory to find the stories behind the numbers. Think of it as the research layer behind this article — open it in a second tab and explore alongside the read. Special thanks to Maciej Polak at PFR Ventures for his assistance in accessing some of the underlying data.A Note on Methodology

On Data Sources: this analysis draws from Crunchbase, CB Insights, Pitchbook, Harmonic, and Dealroom, with Dealroom serving as the primary validation source. Each platform applies different criteria for “unicorn” status, tracks different rounds, and updates at different cadences. Where sources conflicted, I defaulted to Dealroom’s methodology.

On Valuation Opacity: private market valuations are, by definition, private. A company’s “unicorn” status often hinges on a single funding round’s post-money valuation - a number negotiated between founders and investors, not audited or publicly verified. Some companies on this list may trade internally at different prices. Others may have achieved $1B only on paper through structured terms. We may never know who actually invested at what stage, or at what true price.

On Market Categorization: classifying companies into neat verticals is increasingly artificial. Is a drone company “Defense” or “Autonomous/Robotics”? Is a clinical documentation tool “Healthcare” or “AI”? I’ve assigned primary markets based on a rule of thumb, mainly inspired by where their core technology applies - but reasonable people could categorize differently. The lines between AI-native and AI-enabled, between vertical SaaS and horizontal infrastructure, are blurring by design.

On What This Is: this is a trend watch, not a definitive census. It’s an intellectual approximation of where capital is flowing and which technologies are reaching escape velocity in 2025. Treat it as directional signal, not comprehensive registry.

The Numbers at a Glance

1. AI dominates across its entire supply chain

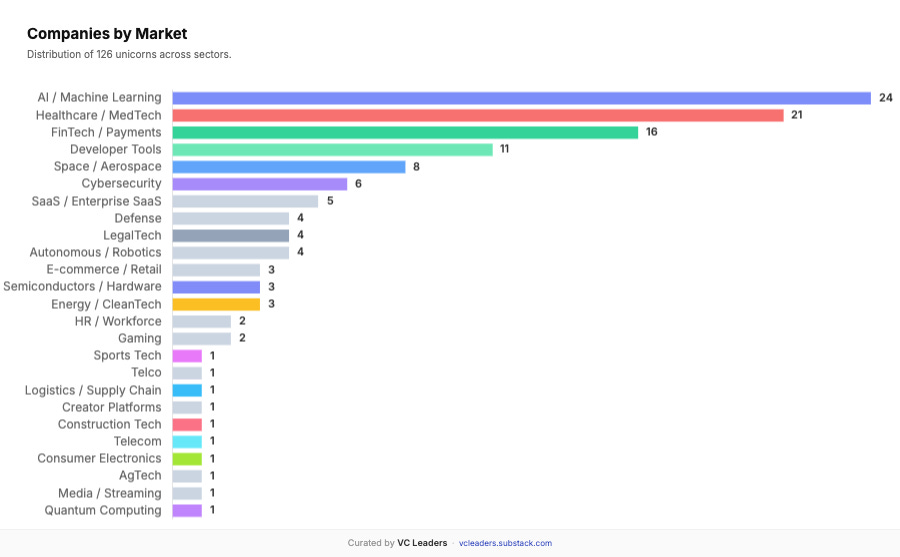

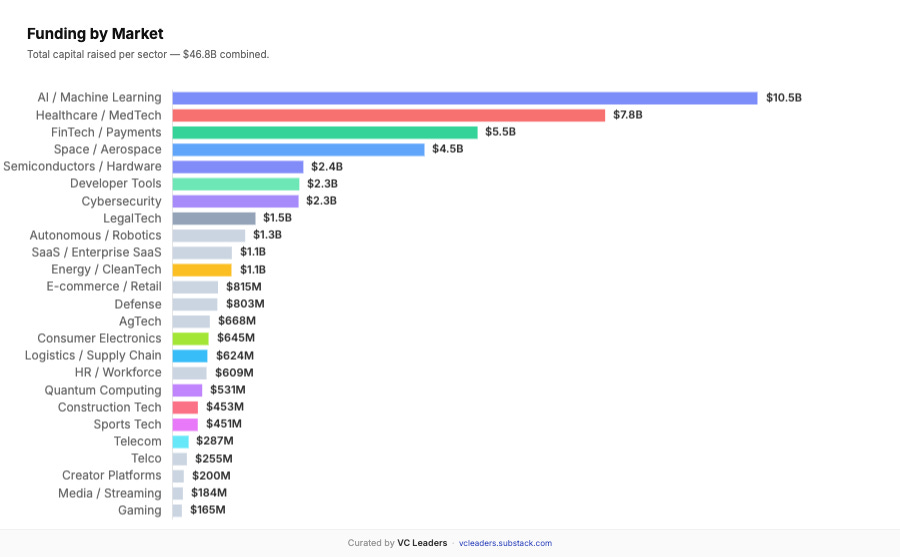

AI / Machine Learning leads the cohort with 24 companies capturing $10.5B in total funding - the largest single sector. When including AI-adjacent categories (Developer Tools, Autonomous/Robotics), the number rises to 39 companies (31%) commanding $14.1B.

But these numbers undersell the story. The distinction between “AI companies” and “companies using AI” has collapsed, and it’s increasingly difficult to exclude any given company from this category. Take LegalTech: an industry that has boomed mainly thanks to AI capabilities introduced into legal workflows - yet we’ve classified it separately from AI/ML. The same logic applies to AI infrastructure plays like Nscale that serves AI compute demand. Include these sectors, and the AI value chain grows to 47 companies (37% of all 2025 unicorns).

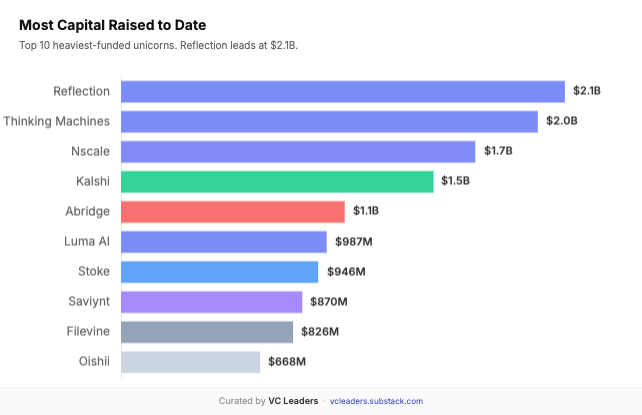

The clearest evidence of the capital concentration: Reflection ($2.13B) and Thinking Machines ($2B) both raised over $2B in their first year - the largest individual raises in the entire cohort. Rather than ask “is it an AI company” it makes more sense to ponder on “where does this company sit in the AI stack”?

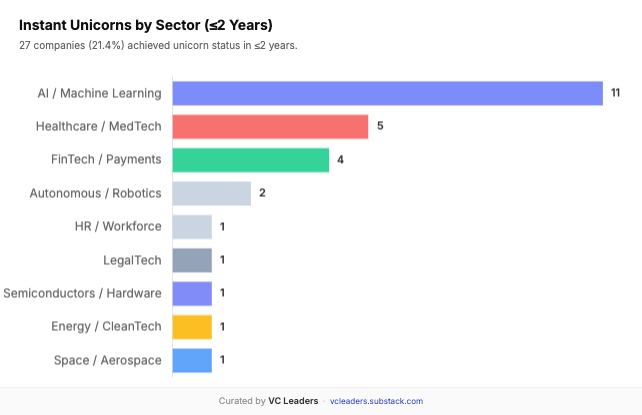

2. The Rise of “Instant Unicorns”

Speaking of the devil, 27 companies (21.4%) achieved unicorn status in ≤2 years from founding, collectively raising $13.1B in total. The 2024-2025 cohort raised an average of $553M (significantly above the overall average) while reaching unicorn status in under two years. This reflects a VC king-making strategy: bold bets on hot-space companies designed to outrun and discourage competition.

Top Instant Unicorns (TTU ≤ 1 year):

Reflection: $2.13B (1 year)

Thinking Machines: $2B (1 year)

Nscale: $1.7B (1 year)

Periodic Labs: $550M (0 years)

Tempo: $520M (0 years)

Unconventional AI: $475M (0 years)

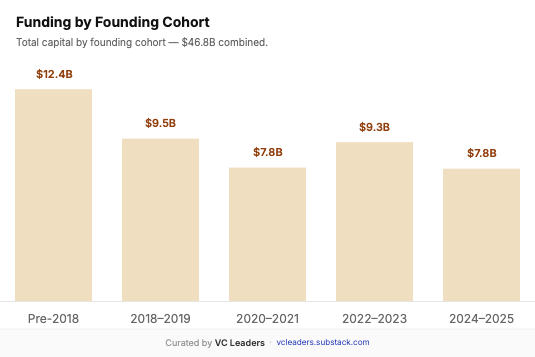

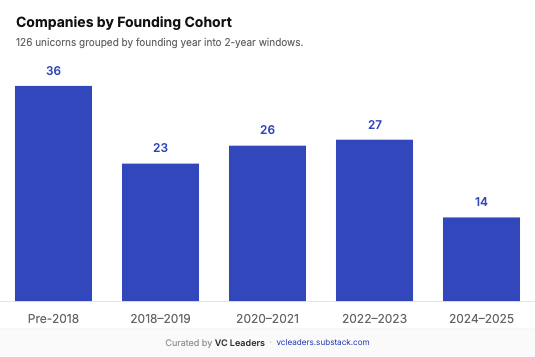

Notably, 36 companies (28%) in the 2025 unicorn class were founded in 2017 or earlier—these are "late bloomers" that took 8+ years to reach unicorn status. The COVID-era produced 26 unicorns but with lower average funding ($300M). The 2024-2025 cohort is smaller but received the largest average checks ($553M), reflecting concentrated bets on AI leaders.

3. DeepTech Renaissance: Space, Semiconductors, Defense, and Quantum Return

17 DeepTech unicorns raised $8.9B at an average of $521M (40% above the overall average). After a decade of “software eating the world,” hard-tech is commanding premium valuations again.

The space sector alone accounts for 8 unicorns and $4.5B in funding in total. This is driven by: reduced launch costs, growing demand for satellite data, and defense/national security applications.

4. The Heavyweights

5 companies raised ≥$1B in total to get to the Unicorn status.

Three of five were started in 2023-2024. The common thread: investors believe these companies can win category-defining positions in multi-trillion-dollar markets (AI foundation models, AI infrastructure, healthcare, prediction markets). $1B+ rounds are reserved for companies with: (1) credible paths to $10B+ outcomes, (2) clear category leadership, and (3) capital-intensive moats (training compute, regulatory approval, network effects).

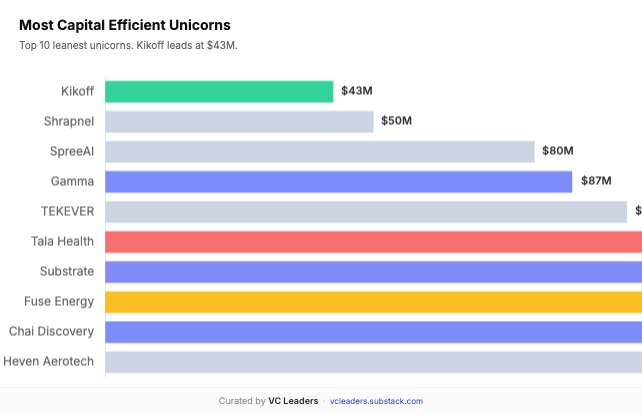

5. The Lean-Unicorn Myth

The VC industry loves the narrative of the capital-efficient startup — the scrappy founder who reaches a billion-dollar valuation on a shoestring budget. Well, you know what they say about myths. 96% (121 of 126) of 2025 unicorns raised $100M or more before crossing the billion-dollar threshold. The median unicorn raised $274.5M across a median of 5 funding rounds.

Only 5 companies in the entire class show disclosed funding below $100M: Kikoff ($42.5M), Shrapnel ($50M), SpreeAI ($80M), Gamma ($87M), and TEKEVER ($97.2M). And even this list deserves an asterisk. Kikoff, which sits at the bottom with $42.5M in disclosed funding across 4 rounds, has not yet disclosed the size of the round that made it a unicorn. When that number surfaces, it will almost certainly push the company well above the $100M mark. The same logic applies to others on this list — when companies appear “lean,” it’s often a matter of timing and disclosure, not genuine capital efficiency.

What the data actually says: Capital Availability > Capital Efficiency.

The path to unicorn status in 2025 is, overwhelmingly, a capital-intensive one. The top 10 most funded companies alone account for 27.1% of total capital raised ($12.7B). Nearly half the class (49.2%) sits in the $200M–$500M band. Building a billion-dollar company almost always requires raising hundreds of millions — and having access to the capital markets to do so. In the VC land, the companies that reach $1B are, almost without exception, the companies that had the capital access to get there.

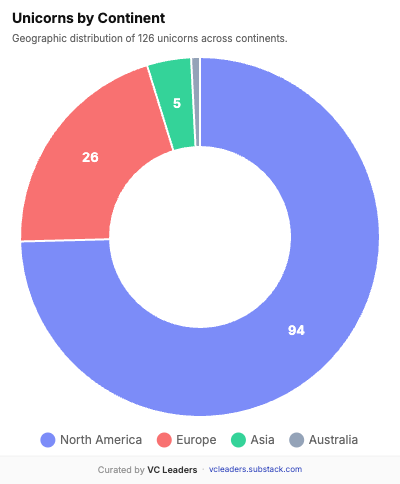

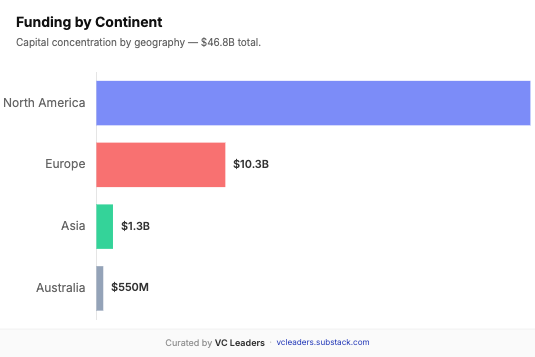

6. Geographic Concentration

The US accounts for 73% of all 2025 unicorns. The UK leads Europe with 8 unicorns, followed by Germany with 5. Singapore notably punches above its weight with 4 unicorns from a small ecosystem. These geographic breakdowns are less meaningful for capital raised, since some of those companies migrated to the US following the availability of funding—so it wouldn't be fair to call them all American companies, though they are based in the US now.

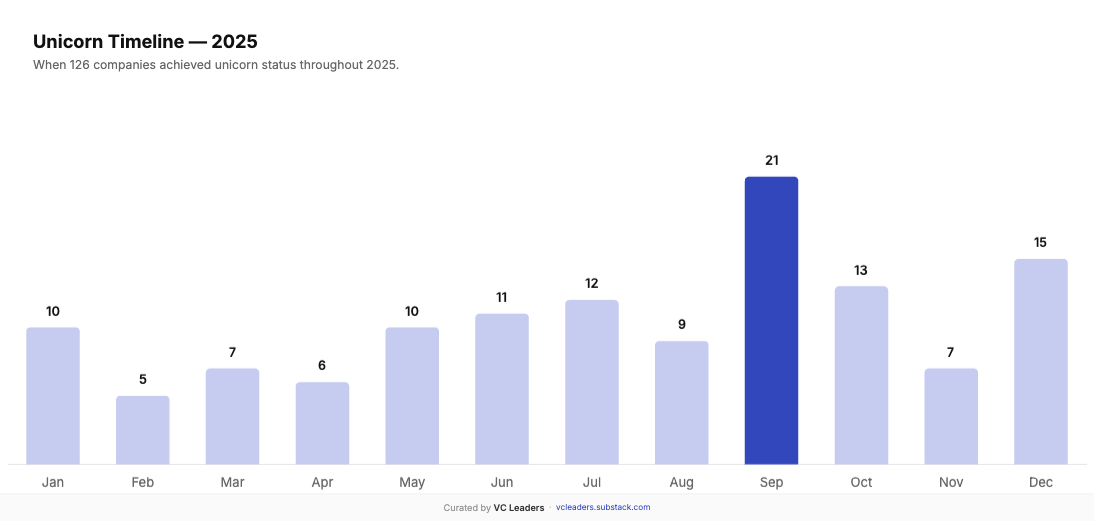

Unicorn Minting Pace

A fun fact: September 2025 was the peak month with 21 new unicorns announced, followed by December (15), October (13), and July (12). This aligns with typical Q3/Q4 funding cycles and year-end portfolio construction.

What this all means?

The 2025 unicorn landscape reveals a fundamental shift in venture capital driven by three major forces: AI dominance, the return of DeepTech, and radically compressed timelines. AI’s dominance is hard to miss. Of the 126 new unicorns, AI touches nearly every category, from foundation models raising $2B+ to healthcare documentation tools. The timeline compression is perhaps most striking. Where unicorns traditionally took 7-10 years to emerge, AI-native companies are now achieving that status in 1-3 years. Some reached unicorn status in under a year, with companies like Reflection and Thinking Machines raising over $2B each within 12 months of founding. Investors are basically front-loading capital to secure category positions before markets crystallize.

Simultaneously, DeepTech is experiencing a renaissance after a decade of software dominance. Space, semiconductors, and defense companies are commanding premium valuations because they offer something software increasingly cannot: defensible moats through capital intensity and technical complexity. The amounts these companies have raised already signal that investors are also willing to pay for that.

The capital strategy bifurcation tells the real story. Some unicorns raised under $100M through exceptional capital efficiency, while others raised $2B+ to dominate emerging categories. What’s disappeared is the middle ground: moderate pace with moderate capital no longer works, at least if you have unicorn-level-ambition. Companies either move with extreme efficiency or raise war chests to establish category leadership. Both paths succeed, but the choice must match market opportunity.

For investors, this means recalibrating how they work around compressed timelines and recognizing that infrastructure plays, the picks and shovels of AI and DeepTech, are capturing disproportionate value. The alpha opportunity lies in identifying the next wave before megafunds arrive: AI infrastructure layers, overlooked DeepTech categories, and capital-efficient plays that can reach unicorn status quickly.

The market is fundamentally transitioning. The old rules and traditional milestones are dead.

Analysis based on 126 companies achieving unicorn status in 2025. Data compiled from Crunchbase, CB Insights, Pitchbook, Harmonic, and Dealroom (primary source of truth).

Special thanks to Maciej Polak at PFR Ventures for his assistance in accessing some of the underlying data.