What does the 2025 IPO pipeline mean for the European VC industry?

Part 1 of our deep dive to European VC-backed IPO pipeline

After the euphoria of 2021-2022, the war in Ukraine and its economic impacts have ushered in a period of uncertainty, if not outright pessimism. Interest rates are rising, people are more aware of global risks, and cash flow is a genuine concern. VCs are under pressure to show real results, not just on paper. Having real money in a bank account is once again seen as the best sign of success. But where does the money come from?

European VCs need (large) exits

There's a simple truth often overlooked in the venture landscape: returns come from exits, and those exits primarily take the form of M&A deals and IPOs. The generated returns are passed on to LPs, and if they are satisfied with the outcomes, they will reinvest. Conversely, if LPs do not receive the expected distributions or have to wait longer than anticipated, it’s no surprise that they hesitate to invest again. This applies to most asset classes, but venture capital stands out for a couple of reasons.

To survive in the industry VCs need to raise funds well in advance of seeing final results of their previous work, usually every 3 to 5 years. This is essential not only to continue making investments—since investment periods for VC funds in Europe typically last three to five years—but also to cover ongoing expenses through management fees. To convince LPs things are looking good, GPs often default to reporting metrics like TVPI (Total Value to Paid-In Capital) to show how much a VC fund is worth on paper compared to how much money LPs have invested in it. By now, though, most LPs know the volatility levels well enough to ignore it.

Consequently, there has been a renewed focus on DPI (Distributed to Paid-In Capital). DPI is an important metric that shows how well a VC fund returns money to its investors. It measures cash distributions against the invested capital. While that sounds straightforward, it can be quite complicated. Reaching solid conclusions about DPI in Europe is very difficult. The data we have is limited and not easy to compare across different markets. Factors like investing in various currencies (think EUR vs GBP vs USD), different reporting standards, and the significant differences between seemingly similar markets (for example, seed deals in Poland compared to those in the UK) all complicate the conclusions.

That being said, if we look at the United States, where data on DPI is compiled by large private platforms, some recent reports suggest that newer funds are producing lower DPI compared to older ones. In other words, VCs are getting worse at their game. For example, only 9% of funds from 2021 delivered some DPI after three years, whereas 25% of funds initiated in 2017 did. After five years, 59% of the 2017 funds had returned capital, compared to just 39% of the 2019 funds. This trend persists with more recent vintages; the 2020 funds are behind after four years, and the 2022 funds lag after two years. This is concerning.

")

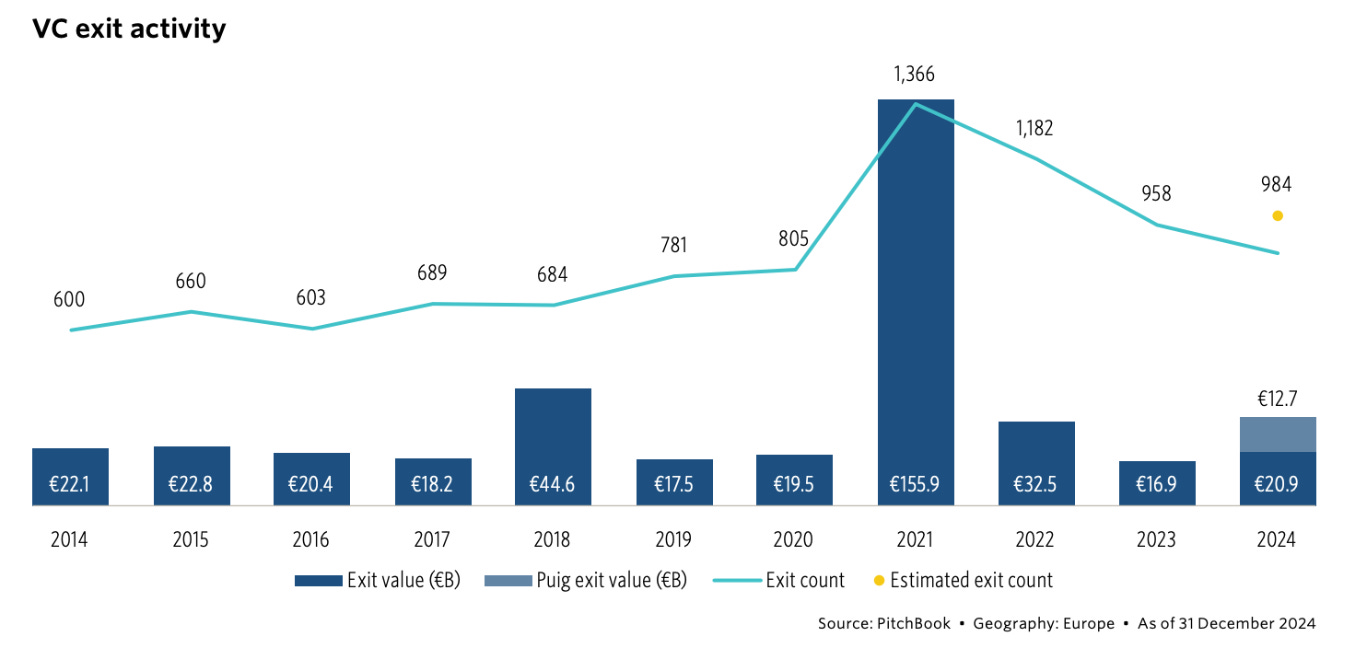

2024 was not a bad year for exits, but it wasn’t good either

In its annual report for 2024, Pitchbook declared that this year would be marked by exit comebacks. The number and value of exits in Europe increased year over year, even when excluding the notable IPO of the Spanish beauty company Puig, which is approximately 12 billion EUR. However, these figures only match the total amount raised by VCs this year. Furthermore, they fall short of the spectacular results seen in 2021, which many hoped would represent a new norm.

The culprit? A significant drop in valuations in both public and private markets during 2022-2023. Many companies and their investors have had to face lower funding rounds or postpone exits, all while hoping for a future recovery. Some have chosen to stay private longer, believing that the scrutiny and regulatory environment of the capital markets would slow their progress, particularly as more private capital is available for late-stage investments. These companies can continue raising money privately and avoid public scrutiny for an extended period.

In addition, acquisitions of large venture capital-backed firms have faced regulatory scrutiny from organizations like the Federal Trade Commission, which has impeded Big Tech acquisitions that are often regarded as the norm in the market. To add to the complexity, this scrutiny coincides with a significant technological shift, where AI tools are now challenging the primary business model traditionally supported by venture capital, namely Software as a Service (SaaS). This swift transformation has sparked concerns regarding the long-term stability of companies that are either being acquired or going public.

VC is JUST another asset class, and there are alternatives

If we take a moment to step outside our bubble, we'll see that venture capital is simply another asset class vying for investors' interest. The competition is getting tougher. Public markets are easier to access, better researched, and much more liquid. In 2024, US equities posted impressive performance, with the S&P 500 achieving total returns of 23.31% and the Nasdaq composite soaring by 28.64%, driven by the persistent growth of mega-cap stocks and striking valuations in the AI sector.

The year 2024 was also a strong one for cryptocurrencies, demonstrating impressive price growth and increasing popularity. Bitcoin captured attention as its price exceeded €50,000 and crossed the significant threshold of €100,000. Bitcoin's value surged by over 135%! Meanwhile, Ethereum experienced growth of more than 55% during the same period. This surge in interest was mirrored by substantial net inflows of $44 billion into global crypto funds.

In European private equity fundraising, the capital raised remained steady compared to 2023 and was near the peak of 2021. However, the number of funds saw a sharper decline, dropping to 127 from 179 the previous year. This trend indicates a market consolidation, with LPs favoring established managers and adopting stricter due diligence amidst a more uncertain macroeconomic landscape.

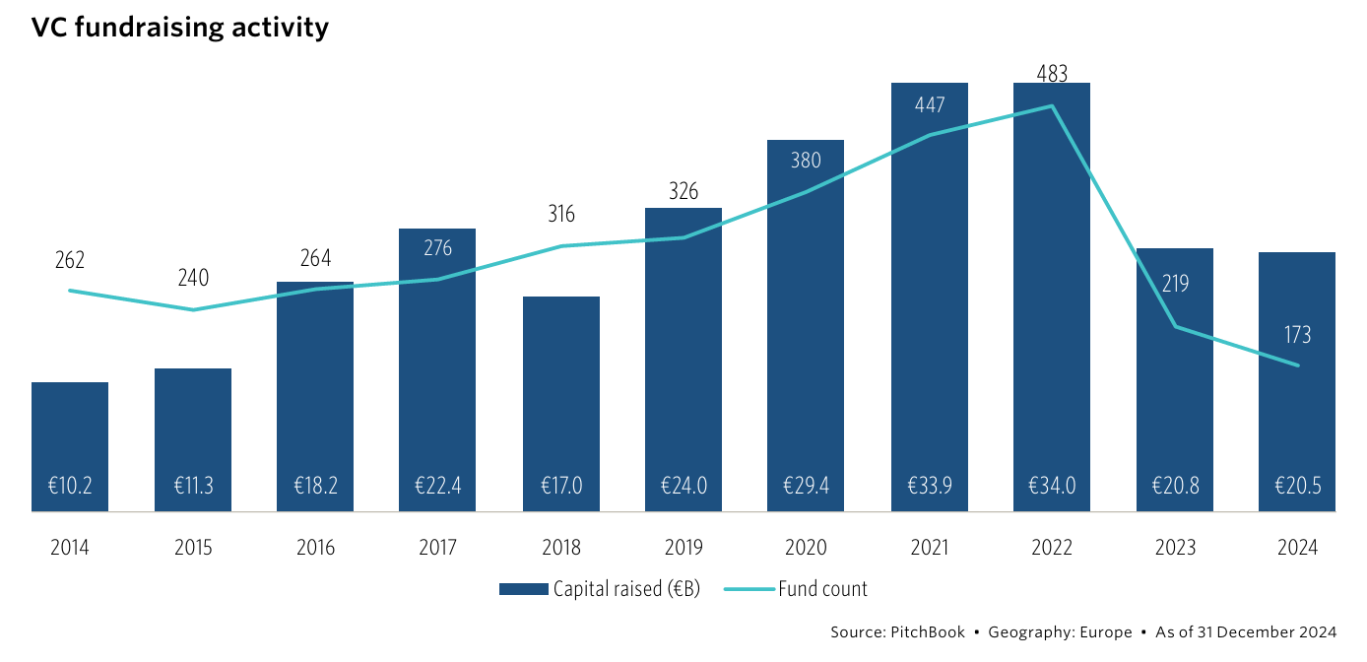

VC fundraising presents a different story. Between 2014 and 2022, European VC fundraising showed steady growth, increasing from €10.2 billion to a high of €34 billion in 2022, accompanied by a rise in the number of funds from 262 to 483. However, in 2023, this trend sharply reversed, with capital raised dropping to €28.0 billion and the number of funds declining to 219. This downward trend persisted into 2024, with €20.5 billion raised from 173 funds, indicating a growing caution among LPs, fewer large fund closures, and increased selectivity. Overall, European VC fundraising declined by nearly 40% from 2022 to 2024.

Last, but not least, we need to mention the bifurcation in VC. In the US, the top 30 VC funds secured 75% of all LP investments. The situation appears even more concerning in Europe, where merely 10 funds accounted for about 50% of the total capital raised by VC funds last year.

What’s the purpose of examining IPOs?

In such a difficult market, every VC-backed exit matters to the overall sentiment. Obviously, it is easier to foresee a potential IPO than a potential M&A, for two reasons: first, companies often gauge investor interest by leaking some information about it to the press; and second, reaching a certain size also limits your other exit options.

We’re also focused on large IPO outcomes as they can significantly impact the entire European VC ecosystem. Successful exits enable VCs to reinvest, attract more LPs to this asset class, and help numerous employees achieve wealth, leading them to start angel investing or launching their own ventures.

A recent list by Dealroom identifies the top 100 IPO candidates in Europe, highlighting firms with approximately $432 billion in private market valuations. This amount is nearly double the total raised by European venture capitalists in the last decade, which is around $250 billion, according to Pitchbook (reported in February 2025 dollars). While we don't believe that all of these will materialize and deliver on their promise (after all, from 2012 to 2023, all of the US tech IPOs after Facebook generated just about $700 billion in market cap), even a fraction of this figure could free up much-needed resources for the European VC ecosystem.

Considering this, in the coming weeks, we will explore the pipeline of potential tech IPOs in Europe for 2025, beginning with Bitpanda, Staffbase, Revolut, and Bolt. l

Bitpanda: Europe’s crypto darling

Founding year: 2014

Location of HQ: Vienna, Austria

Total funding: €450 000 000

Employment growth y/y: 19%

Number of employees: 705

Short description: a digital investment platform that democratizes access to cryptocurrencies, stocks, and other digital assets.

Bitpanda's IPO is expected to draw significant interest, particularly in the European Union and the Austrian market. As a major player in cryptocurrency trading, its success will reflect investors' sentiments not only about crypto but also about the potential of crypto projects in the EU. Recent changes in the views of key US stakeholders regarding crypto, combined with the rising number of crypto investors in the past year, suggest that a successful IPO could mark a positive shift for the crypto market in Europe, encouraging more investment in the EU's expanding crypto industry. Conversely, if the IPO receives a lukewarm response, it could indicate continued concerns about the health and future of the crypto market in the EU.

A successful IPO for Bitpanda, lastly valued at over $4 billion, would be a landmark event for the entire European crypto sector and particularly significant for the Austrian ecosystem. The potential windfall for Vienna-based investors like Speedinvest, Elevator Ventures, and UNIQA Ventures is especially noteworthy. As Speedinvest and Elevator have both raised subsequent funds in the recent past, there is a strong possibility that both have used Bitpanda's success as a compelling argument for their limited partners. In smaller ecosystems like Austria, the presence and financial performance of companies like these establish the groundwork for future success stories, not only in financial terms but, more importantly, in shaping the overall narrative of the tech sector.

Bitpanda recently received approval from the UK regulator FCA and secured the MiCAR license from Germany's BaFin. It announced that with these licenses, it is now ready "to bring regulated services to all 450 million EU citizens." This certainly sounds like a promising lead-in to a potential IPO equity story.

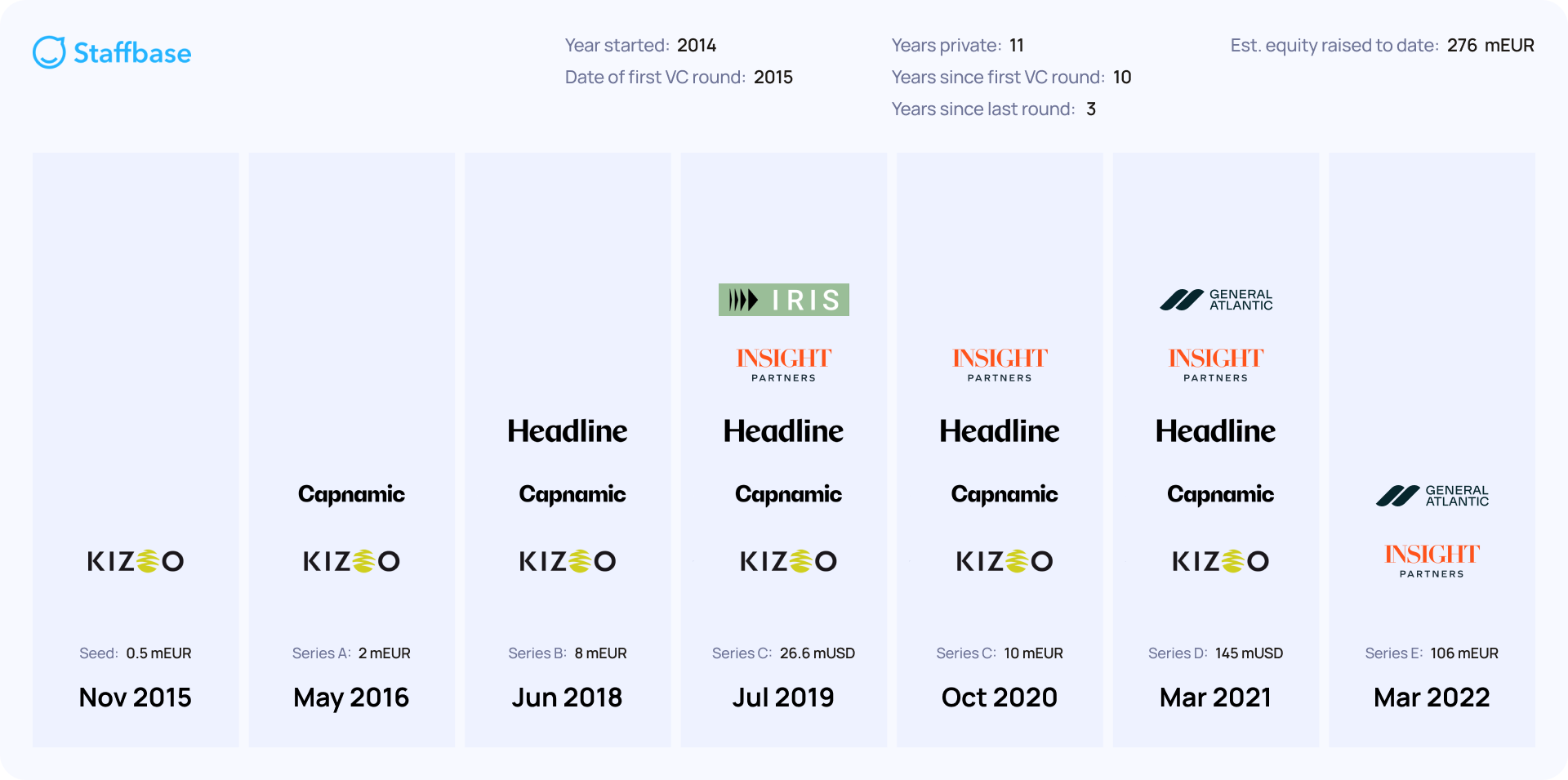

Staffbase: does anybody love SaaS in Europe anymore?

Founding year: 2014

Location of HQ: Chemnitz, Germany

Total funding: €276 000 000

Employment growth y/y: 6%

Number of employees: 866

Short description: leading provider of employee communications platforms, enabling companies to connect with their workforce through mobile-first solutions.

Staffbase's potential IPO carries significant implications for the broader Software-as-a-Service (SaaS) industry. As one of the most promising startups in the German market, its performance might be closely examined not only by numerous other SaaS companies, especially those targeting similar enterprise business models, but also by fellow German unicorns. A strong debut could validate that market opportunities still exist for such SaaS businesses. A successful IPO will also help counter the competition posed by new AI-driven, super-tailored software solutions. Conversely, a subpar performance could spark concerns about market saturation or investor interest in SaaS offerings in the current technological landscape. Therefore, Staffbase's IPO will act as an important bellwether, providing valuable insights into market conditions and investor sentiment towards the SaaS sector as a whole.

Staffbase has announced plans to IPO as early as December 2024, suggesting that it may not utilize the 2025 windows for its initial public offering. Interestingly, the company still retains a strong presence in Chemnitz, a city in Eastern Germany with just over 200,000 inhabitants in the heart of Saxony. This area has relatively few success stories, presenting a significant opportunity to increase the density of success stories in this part of Germany.

Bolt: A Beacon for CEE and a Testament to Big Outcomes

Founding year: 2013

Location of HQ: Tallinn, Estonia

Total funding: €1 500 000 000

Employment growth y/y: 25%

Number of employees: +12k

Short description: European mobility platform offering ride-hailing, micro-mobility (scooters and e-bikes), and food delivery services.

Bolt's upcoming IPO is highly significant for the Central and Eastern European (CEE) region and the Nordics. If successful, it could signify a pivotal shift, demonstrating the ability of CEE-based tech companies to scale effectively and attract substantial global investment. Although Bolt is already a prominent global tech player, a successful IPO could further bolster the ecosystem, particularly through a new wave of founders in the area, and draw more venture capital, potentially transforming the CEE tech landscape. Therefore, Bolt's IPO represents not only one company's journey; it encapsulates the potential of an entire region to make impactful contributions on the world stage and inspire increased investment in CEE and Nordic startups from both local and international investors.

Bolt's notable investors include early entrant Mercedes-Benz Group and venture capital firms such as Creandum and Korelya Capital, which joined at Series C with a $1 billion valuation. Sequoia Capital, a prominent global venture firm, led Series E and F, underscoring Bolt's global appeal and growth trajectory. D1 Capital Partners, known for its investments in later-stage companies, participated in several rounds, including Series D at a $3.5 billion valuation and Series E.

Revolut: A shining star of fintech going mainstream

Founding year: 2015

Location of HQ: London, UK

Total funding: €1,600,000,000

Employment growth y/y: 49%

Number of employees: +17k

Short description: financial technology company offering banking, payments, and investment services through a mobile app.

Revolut's eventual IPO marks a pivotal moment for the fintech sector, especially within the UK's robust fintech landscape. Recognized as one of Europe's most valuable private companies and a significant UK success story, its performance in public markets will be scrutinized as a reflection of investor confidence in the sector's development, both internationally and locally. Moreover, as one of the largest companies to go public after crowdfunding, Revolut's success might rekindle interest in crowdfunding and encourage more retail investors to engage in the market.

Revolut's rise has been propelled by a variety of investors, from early supporters like Balderton Capital, Index Ventures, and Seedcamp, who invested in seed and Series A rounds, to later-stage powerhouses like DST Global and TCV. Tiger Global and SoftBank Vision Fund spearheaded the Series E, signaling elevated expectations. Even Mastercard has expressed interest. This blend of early-stage VCs, growth investors, and strategic partners showcases Revolut's wide appeal.

New Funds

🇧🇪 Junction Growth Investors - €115M - Fund Close

Junction Growth Investors, a Belgium-based venture capital firm founded in summer 2022 by Bruno Vanderschueren (ex-Lampiris), Pieter-Jan Mermans (ex-REstore), Dirk Dewals (ex-Gimv), and Vincent Gregoir (ex-Inven Capital), has closed its first fund at €115 million. The fund focuses on energy transition sectors, including grid-enhancing technologies, sustainable buildings, energy management systems, and industrial decarbonization. Notable LPs include family offices like the owners of AB-Inbev and Umicore, European Investment Fund (EIF), BNP Paribas Fortis Private Equity, PMV, Belgian Growth Fund, Keeling Capital, and technology entrepreneurs such as Jan-Willem Rombouts, Gregoire de Streel, and Jean-Guillaume Zurstrassen. Junction Growth Investors has already made seven investments, including Ampacimon (BE), Eneida (PT), Eturnity (CH), and EET (AT), aiming to support sustainable growth and innovation across Europe.

🇪🇸 Nina Capital - €50M - First Close

Nina Capital has launched its €50M Fund III, targeting early-stage healthtech startups across Europe, North America, Israel, and Australia. The fund aims to invest in pre-seed to Series A companies, with initial investments ranging from €250K to €1.5M each. Founded by Marta-Gaia Zanchi and Marc Subirats, Nina Capital focuses on innovations in diagnostics, medical devices, healthcare infrastructure, and clinical workflow automation. The first investment from Fund III is Sonar Mental Health, a US-based mental health platform leveraging AI and human-led support.

New Rounds

🇩🇪 Accure Battery Intelligence - $16M - Series B

Accure Battery Intelligence, an Aachen-based AI-driven battery safety and performance company, has raised $16M in Series B funding led by Incharge Capital Partners, with participation from BlueBear Capital, HSBC Asset Management, Riverstone Holdings, Capnamic, and 42CAP. Accure develops products that prevent thermal runaway events, reduce downtime by anticipating maintenance needs, accurately assess battery health and state of charge, and help operators maintain warranty coverage—making batteries more bankable and insurable. Their AI-based predictive analytics software ensures battery safety, reliability, and maximum output for energy storage systems and EV fleets worldwide.

🇸🇪 Agteria Biotech - €6M - Seed

Agteria Biotech, a Swedish startup dedicated to reducing methane emissions from cattle, has raised €6 million in seed funding. The round was led by Industrifonden and AgriZeroNZ, with continued support from existing investors Norrsken Launcher and Mudcake. Agteria has developed a patent-pending molecule that significantly lowers methane emissions from cattle, offering a scalable and cost-effective solution to address agricultural greenhouse gas emissions.

🇸🇪 AI-BOB - €2M - Seed

AI-BOB, a Stockholm-based constructiontech startup, has raised €2 million in a seed funding round led by CapitalT, with participation from Fund F, NCA, and several angel investors. The company leverages AI to ensure construction projects comply with regulations and environmental requirements by analyzing blueprints and detecting errors early.

🇮🇹 Akamas - €9.6M - Seed

Akamas, a Milan-based startup specializing in AI-driven cloud optimization, has raised €9.6M in a seed funding round led by United Ventures. The funding will support Akamas’ expansion into the US market by opening its first office in Boston and scaling its team from 10 to 35 employees. The company aims to establish itself as a leader in full-stack optimization for cloud and Kubernetes environments. Akamas’ parent company, Moviri group, will maintain a strategic minority position while transitioning operational control.

🇬🇧 Applied Monitoring - £500K - Seed Extension

Applied Monitoring, a Sunderland, UK-based company developing a healthcare and fitness monitor, has raised an additional £500K in seed extension funding led by Mercia Ventures’ North East Venture Fund. The startup has created a non-invasive method to monitor lactate levels in blood, aiding athletes in tracking peak exertion and optimizing training regimes.

🇵🇱 Bethink - €5.9M - Seed

Polish startup Bethink has secured €5.9M in seed funding led by TDJ Venture, with participation from angel investor Paweł Maj. Bethink develops personalized e-learning platforms for high school and medical education, utilizing proprietary atomic content technology and social learning features. With over 20,000 users and revenue exceeding €4.5M in 2024, the funding will support team expansion, the launch of a mathematics learning platform, and preparations for international growth.

🇧🇪 Bioxodes - €2.7M - Series A Extension

Bioxodes, a Gosselies, Belgium-based clinical-stage biopharmaceutical company, has raised €2.7M in Series A extension funding. The company focuses on developing RNA-based therapeutics targeting cancer, autoimmune conditions, fibrosis, and infectious diseases.

🇸🇪 Bluebook - €2.4M - Pre-Seed

Stockholm-based Bluebook, an AI-powered accounting software for firms, has raised €2.4M in a pre-Seed funding round led by EQT Ventures and Y Combinator. Participating angel investors include Huey Lin (Founding COO of Affirm), Laura Modiano (OpenAI), and Carles Reina (Eleven Labs). The funding will support Bluebook’s expansion in the Nordics and Europe, enhancing their AI platform to automate accounting tasks and enable firms to focus on high-value advisory work.

🇬🇧 Clear Decisions - Undisclosed - Pre-Seed

Clear Decisions, a London-based startup specializing in AI-driven compliance and sustainability solutions for data centres, has raised an undisclosed amount in a Pre-Seed funding round led by SFC Capital.

🇳🇱 Collie - €3.5M - Seed

Collie, a Dutch livestock management startup, has raised €3.5M in seed funding from Freigeist Capital. The company offers a digital livestock management solution using specialized collars and an accompanying app, enabling farmers to create virtual fences and guide their herds remotely. This replaces the need for physical fencing, optimizing grazing practices, reducing labor costs, and improving pasture management and soil health. Farmers using Collie have reported significant cost savings on feed, reduced time spent on herding, and increased grass production.

🇨🇿 Edmund - €500K - Pre-Seed

Edmund, a Czech AI startup, has raised €500K in a pre-seed funding round led by Lighthouse Ventures, with participation from Czech Founders VC, Borovicka Capital, and Tensor Ventures. The company brings AI to the factory floor by addressing manufacturing's biggest data challenges, enhancing troubleshooting and maintenance processes through its innovative platform.

🇨🇭 ETFbook - €4M - Series A

ETFbook, a Zurich-based data and analytics platform specializing in the ETF market, has raised €4 million in Series A funding led by BlackFin Capital Partners, with participation from business angels. The company offers a comprehensive ETF data and analytics platform accessible through a web app and APIs, serving over 35 institutional clients across key European financial hubs including London, Paris, Frankfurt, Amsterdam, and Dublin.

🇪🇸 Exoticca - €25M - Venture Debt Facility

Exoticca, the Barcelona-based travel tech platform for multi-day tour packages, has secured an additional €25M in a Venture Debt Facility from BBVA Spark. This funding complements its recent €60M Series D equity round led by Quadrille Capital, with participation from new investors such as Acurio ICF and existing investors including 14W, Mangrove, Bonsai, Sabadell, and Aldea. Bringing the total funding from this round to €85M, Exoticca is advancing its AI-driven platform that develops sophisticated algorithms to interconnect all components of connected trips, synchronize services, personalize travel recommendations, optimize pricing strategies, and automate complex itinerary creation.

🇹🇷 Fal.ai - $49M - Series B

Fal.ai, a Turkish startup specializing in AI-generated media for enterprise use, has raised $49M in a Series B funding round led by Notable Capital, with participation from Andreessen Horowitz, Bessemer Venture Partners, Kindred Ventures, and First Round. Founded in 2021, Fal.ai serves enterprises like Quora, Canva, and Perplexity.

🇫🇷 Germitec - $30M

Germitec, a France-based MedTech company specializing in UV-C disinfection solutions, has secured $30M in a financing round led by Eurazeo, with participation from existing shareholders and the company’s management team. Germitec’s UV-C devices are designed to prevent healthcare-associated infections by providing chemical-free disinfection solutions effective in operating rooms, medical equipment, and reusable instruments.

🇨🇿 Grid.online - €1.5M - Seed

Czech startup Grid.online has secured €1.5 million in seed funding led by Reflex Capital, with participation from J&T Ventures and Grid Invest. The company offers a shared courier network operating as a logistics cloud, allowing businesses to access delivery capacity on demand while increasing earning opportunities for couriers. Founded in 2024 the company addresses high costs and inefficiencies in parcel delivery for businesses.

🇪🇪 Gridraven - €4M - Seed

Gridraven, a Tallinn-based startup, has secured €4 million in seed funding led by 42CAP and Icebreaker.vc. The company's AI-driven Dynamic Line Rating technology addresses grid bottlenecks, unlocking up to 30% more grid capacity annually without additional hardware. This funding will support scaling operations, expanding the team, and accelerating the rollout of their innovative solutions in the US market, starting with Austin, Texas. Gridraven's software optimizes transmission lines by leveraging machine learning-based weather models, allowing grids to carry more power during favorable conditions and enhancing overall energy efficiency.

🇬🇧 HowNow - £7.5M - Series A

London-based AI-powered learning and skills platform HowNow has completed a £7.5 million Series A funding round led by Mercia Ventures and Pearson. Building on previous investments from these partners earlier in 2023, HowNow aims to help businesses and teams upskill, share knowledge, and access relevant learning resources efficiently. Headquartered in London, the platform serves notable clients including TomTom, MoneyBox, Bausch & Lomb, UKTV, and Good Energy, and collaborates with Pearson to deliver the UK Government's Learning and Skills Platform.

🇩🇪 Integral - €6.3M - Seed

Berlin-based fintech startup Integral has secured €6.3M in seed funding led by General Catalyst and Cherry Ventures, with participation from Puzzle Ventures and various European entrepreneurs. Integral aims to streamline accounting, taxation, and payroll for SMEs across Europe with its AI-powered platform that integrates collaboration tools with human tax advisors and financial system integrations.

🇬🇷 Keragon - €7.2M - Seed

Greek-founded and NY-based Keragon, an AI-powered healthcare automation platform, has secured €7.2M in a seed funding round led by Upfront Ventures, with participation from Afore Capital, Focal, and 25m Health. Keragon offers a HIPAA-compliant, no-code workflow automation system that seamlessly integrates over 300 healthcare tools, significantly reducing manual work and enhancing operational efficiency for healthcare providers. Since launching in June 2024, the platform has surpassed 100 paying customers, achieved a 30% month-over-month growth rate, and executed over 2 million workflow automations.

🇸🇪 Kodiak Hub - $6M - Seed

Kodiak Hub, a Stockholm-based AI-powered supplier management platform, has raised $6 million in a seed funding round led by Oxx Ventures. The company plans to expand its operations into the United States, helping American businesses build more resilient and sustainable supply chains. Kodiak Hub utilizes AI to analyze supplier performance, reducing onboarding time by 80% and improving supplier engagement by 90%.

🇩🇪 Lanch - €26M - Series A

Germany-based Lanch has raised €26M in Series A funding led by Felix Capital and HV Capital. The startup leverages social media and influencer partnerships to develop and distribute fast-food brands like Loco Chicken and Happy Slice Pizza. Since launching commercially 18 months ago, Lanch has expanded to 350 ghost kitchens and partnered with major influencers.

🇬🇧 Latent Labs - $50M - Series A

Latent Labs, founded by former DeepMind scientist Simon Kohl, has launched from stealth with $50 million in Series A funding. The round was co-led by Radical Ventures and Sofinnova Partners, with participation from Flying Fish, Isomer, 8VC, Kindred Capital, Pillar VC, and notable angels including Jeff Dean (DeepMind’s chief scientist), Aidan Gomez (Cohere founder), and Mati Staniszewski (ElevenLabs founder). Latent Labs is developing AI foundation models to “make biology programmable,” aiming to partner with biotech and pharmaceutical companies to generate and optimize proteins.

🇪🇸 Libeen - €25M - Seed

Libeen, a Madrid-based smart housing startup, has secured €25 million in a seed funding round led by Andbank through MyInvestor and Actyus (Andbank Group companies), with participation from Cusp Capital, angel investors Íñigo Juantegui (co-founder of La Nevera Roja), Enrique Linares (co-founder of Letgo), and Juan Velayos (founder of JV20). The company offers a flexible rent-to-own model designed to make homeownership more accessible for Gen Z by allowing monthly rent payments to build equity towards purchasing a home.

🇳🇱 Mair Therapeutics - Undisclosed - Pre-Seed

Mair Therapeutics, a Netherlands-based biotechnology startup, has raised an undisclosed amount in Pre-Seed funding led by Torrey Pines Investment. The company is focused on discovering compounds that regulate the lysosomal ion channel TMEM175, aiming to treat neurodegenerative disorders such as Parkinson’s disease.

🇱🇺 MarketLeap - $8M - Series A

MarketLeap, a Luxembourg-based AI-driven platform for D2C ecommerce, has closed an $8M Series A funding round led by Smedvig Ventures, with participation from Expon Capital, Motier Ventures, and business angels including former executives from Amazon, SoftBank, and Unilever. The company’s platform manages various aspects of online selling, including marketing, logistics, compliance, and fulfillment, allowing brand owners to focus on product development. With this new capital, MarketLeap plans to accelerate platform development and expand its customer acquisition efforts, enhancing features like inventory management, pricing automation through LLMs, and advanced data processing.

🇹🇷 Mundi - $2.5M - Seed

Mundi, an Istanbul-based fintech startup, has raised $2.5M in a Seed funding round led by Speedinvest and DeBa Ventures. The company is developing a capital markets platform designed to make investment opportunities more accessible to Turkish SMEs. By collaborating with financial intermediaries, Mundi enables businesses to automate savings management through solutions like overnight savings accounts, mutual funds, and repo products, ensuring efficient fund allocation while maintaining regulatory compliance.

🇩🇪 neurocare Group - €19.3M - Seed

neurocare Group, a Munich-based provider of a mental health platform, has raised €19.3M in seed funding led by Impact Expansion and TVM Capital Healthcare. The company plans to use the funds to further develop its technologies and expand its international footprint of mental health clinics. Neurocare empowers clinicians to provide personalized treatment for a range of psychological and neurological conditions through its cloud-based solution, integrating innovative methods like sleep hygiene, rTMS, QEEG, and neurofeedback alongside traditional approaches such as talk therapy and pharmaceuticals.

🇮🇹 Newronika - €13.6M - Series B

Newronika, a Milan-based deep brain stimulation company, has raised €13.6M in Series B funding led by Fondazione ENEA Tech Biomedical, with participation from existing investors Indaco Venture Partners SGR, Innogest SGR, Wille Finance, TNBT Capital, and F3F. Newronika aims to enhance treatments for Parkinson’s disease by delivering precision therapy through real-time patient data.

🇨🇭 Nextesy - €3.5M - Pre-Seed

Nextesy, a Swiss AI startup with Balkan roots, has raised €3.5 million in pre-seed funding led by Fifth Quarter Ventures, alongside business angels. Founded in 2023, the company develops an AI-powered platform that automates complex administrative processes, eliminating repetitive tasks and improving efficiency by over 30% for SMEs.

🇪🇸 Nido - €5M - Seed

Nido, a Spanish aerothermal platform, has secured €5M in seed funding to accelerate its AI-driven platform for the design and installation of residential aerothermal systems. The round was led by Iberdrola and Ship2B Ventures, with participation from Zubi Labs, Decelera Ventures, Silence VC, and institutional investors including Instituto Valenciano de Finanzas (IVF), the City of Valencia, and ENISA, alongside 15 business angels. Nido’s platform utilizes 3D modeling and artificial intelligence to optimize the design and installation processes, streamlining operations for installers, suppliers, and customers.

🇵🇹 Noxus - $1.5M - Pre-Seed

Noxus, a Portuguese SaaS platform, has raised $1.5M in pre-Seed funding led by SFC Capital, with participation from Antler, Bynd VC, Caixa Capital, AltaIR Capital, I2BF Global Ventures, Yellow Rocks, and Smart Partnership Capital, alongside business angels. The platform empowers enterprises to build and deploy their own AI workforces, offering AI-powered process automation and tools for managing AI workflows while ensuring data privacy and security.

🇬🇧 OneID - £16M - Seed

OneID, a London-based provider of bank-verified digital identification services, has raised £16M in funding. The round was led by ACF Investors, with participation from over 200 UK, Swedish, and US angel investors. OneID offers digital identity verification through bank-verified data, enabling a document-free process completed within twelve seconds. This approach prioritizes privacy and helps businesses streamline onboarding, increase sales, reduce operational costs, and mitigate fraud risks.

🇬🇧 Plain - $15M - Series A

Plain, a UK-based customer support platform founded by ex-Deliveroo employees, has raised $15M in Series A funding. The round was led by Battery Ventures, with continued participation from Connect Ventures, Index Ventures, and a group of angel investors. Plain's API-first architecture seamlessly integrates with existing company systems, enhancing and streamlining B2B customer support operations.

🇫🇷 Planted - €5M - Seed

Planted, a French green tech startup founded in 2021, has secured €5 million in seed funding to enhance its AI-driven ESG software platform. The investment was led by TechVision Fonds and WENVEST Capital, with participation from neoteq ventures, AWS Gründungsfonds, and Smart Infrastructure Ventures, as well as business angels. Planted's platform assists companies in their sustainability transformations by automating processes such as materiality analysis, carbon accounting, decarbonisation projects, and local environmental protection efforts, significantly reducing the time and effort required for ESG compliance.

🇫🇷 Proba - €1M - Seed

Proba, a French agritech startup, has secured €1 million in seed funding to advance its mission of decarbonizing agriculture through innovative insetting solutions. The company leverages proprietary technology to help farmers optimize crop management and reduce their carbon footprint by embedding sustainable practices directly into their operations. This funding round was led by GreenInvest Capital, with participation from EcoTech Ventures and angel investors.

🇵🇹 Relive - $5.5M - Series A

Relive, a Portuguese proptech platform specializing in tools for real estate agents to rent, buy, and sell properties, has secured $5.5M in Series A funding led by Indico Capital Partners, with participation from Shilling and Bynd. Founded in October 2020 in Lisbon, Relive offers an all-digital mobile platform that enables agents to create, manage, and grow their real estate businesses efficiently.

🇬🇧 Renew Risk - £5M - Seed

Renew Risk, a company specializing in risk modelling and analytics for renewable energy assets, has raised £5 million in a seed funding round led by Molten Ventures, with participation from Lloyd’s of London, Insurtech Gateway, and influential angel investors. The startup bridges the gap between the renewable energy sector and financial markets, providing insights into physical risks such as hurricanes and earthquakes affecting renewable assets like offshore wind farms and solar farms.

🇬🇧 Revving - £107M - Series A

Revving, a UK-based adtech startup addressing delayed payments, has raised £107M in a Series A funding round led by DWS Group, with participation from Awin. The company offers a payment acceleration solution that provides immediate access to earned sales revenue before invoices are raised, helping businesses overcome cash flow challenges in the adtech sector.

🇬🇧 Serene - £930K - Pre-Seed

Serene, a London-based provider of an AI-powered platform developing a consumer vulnerability engine, has raised £930K in pre-seed funding. The round was led by Fuel Ventures, with participation from NatWest Group, Oxford Seed Fund, and a group of angel investors. Serene offers businesses an AI-powered consumer vulnerability engine that combines AI with behavioral insights to detect distress early and provide support to customers.

🇩🇪 Spark e-Fuels - €2.3M - Pre-Seed

Berlin-based Spark e-Fuels has secured €2.3M in a Pre-Seed funding round led by Nucleus Capital, with participation from Zero Carbon Capital, IBB Ventures, Chemovator, Voyagers.io, and 1.5° Ventures. The round also included business angels from Shell, Lufthansa, BP, Siemens Energy, and McKinsey, bringing valuable expertise in energy, aviation, and industrial innovation. Spark e-Fuels is developing scalable and cost-effective sustainable aviation fuel (SAF) production technology. The funding will be used to build its first e-fuel pilot plant and expand its team to accelerate technology development and commercialization, aiming to support the transition to net-zero aviation and broader industrial decarbonization.

🇧🇬 UVIONIX - €3.4M - Seed

Bulgarian-founded UVIONIX has raised €3.4M in a seed round led by LAUNCHub Ventures, with participation from PortfoLion, Underline Ventures, and Robin Capital. The startup is transforming warehouse automation with AI-powered autonomous drones that achieve 99.9% accuracy in real-time inventory monitoring.

🇸🇪 Verigraft - €1.2M - Seed

Swedish biotech startup Verigraft has secured €1.2M in seed funding from Eurostars to advance its pioneering 3D-printed arterial grafts. Verigraft develops customized, biocompatible vascular solutions aimed at replacing damaged arteries, significantly reducing the risk of rejection and improving patient recovery outcomes.

| A guest post by

|